I have a problem here. I bought a printer and before the warranty elapsed it had a problem printing. I returned it and they said they fixed it. I took it but realised that its still doing the same. I returned it for the second time and they still failed for the second time. I returned it for the third time now they want to give me the same printer which I no longer trust as they failed to repair it two times.

I have been communicating with them but they are refusing to assist me. They want me to take the old one saying they have fixed it but they failed two times to fix it. I am calling them every day to talk to the manager and they always say he will call me back but he never does so. I talked to them this morning they said i should collect the old printer which failed so many times,

I call every day and they say the manager is in a meeting or not in and they will pass my message and get back to me but they never get back to me. Please help me.

Section 16 of the Consumer Protection Act says that when a product develops a problem during the warranty period the dealer has a right to decide what they want to do, choosing from three options. They can offer you a repair, a replacement or a refund, the three Rs. Clearly any sensible supplier will choose the simplest and cheapest option for them which is to try and repair the problem. This store had the right to do that and you were right to give them that chance.

However, things change after that. The same section of the Act says that if a supplier repairs something and the same problem reoccurs within the next three months, they then have just two options. They can only replace the item or refund you. There's no second chance to repair it.

I emailed the company and their MD told me that his staff would immediately deal with the issue and contact you to confirm this.

Will I get my money back?

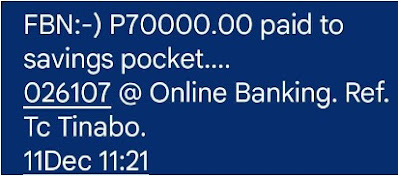

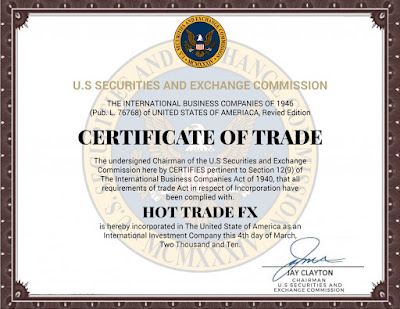

There is this guy he took money from me saying I'm funding his business of being a loan shark. He said he needed money to loan his customers which would come back with interest. He said the initial amount would have a 12.5% compound interest monthly for 6 months. The amount was P5,900 in total which was supposed to give me P11,800. But he only gave me P2,000 so I told him I just wanted my P3,900 since he couldn't manage. There's a dozen of us he didn't pay. I have bank transactions to prove the investment.

Now he blocked me I have no way of communicating.

This is going to be complicated. Very complicated.

Firstly, you're dealing with an industry that is heavily regulated. NBFIRA, the Non Bank Financial Institutions Regulatory Authority oversees the microlending industry and they have extremely strict rules about how micro-lenders are established and how they behave. I wonder whether this guy actually approached NBFIRA and got their advice or approval before setting up his company in such a strange way? I suspect he didn't. I checked and the company doesn't currently appear to be registered with NBFIRA.

I think you should approach NBFIRA and get their advice. As someone who invested in the company, you might need to get their opinions on your status as someone who is a stakeholder in a company that is possibly operating illegally.

I contacted the guy and he made a serious of excuses and claimed that the reason there's a delay is that he's the subject of a court case. He sent me pictures of court receipts which suggest that he's being truthful. However, I don't think that should be your concern.

In your position I would approach the Small Claims Court and see if you and the other people who lent him money can get an order against him for your money.